FAO Cereal Supply and Demand Brief

The Cereal Supply and Demand Brief provides an up-to-date perspective of the world cereal market. The monthly brief is supplemented by a detailed assessment of cereal production as well as supply and demand conditions by country/region in the quarterly Crop Prospects and Food Situation. More in-depth analyses of world markets for cereals, as well as other major food commodities, are published biannually in Food Outlook.

Monthly release dates for 2017: 02 February, 02 March, 06 April, 04 May, 08 June, 06 July, 07 September, 05 October, 02 November, 07 December.

Record cereal production to lift global inventories to an all-time high

Release date: 08/12/2016

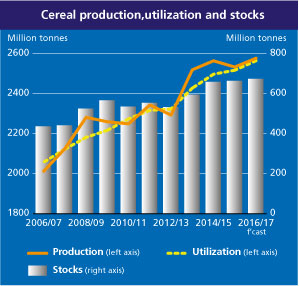

The outlook for 2016/17 global cereal supply situation has received a further boost in recent weeks, owing to generally favourable growing conditions for crops to be harvested later in the season. Accordingly, FAO’s latest forecast for 2016 world cereal production has been raised to 2 577 million tonnes, up 6 million tonnes from November’s figure and 1.7 percent (44 million tonnes) above last year’s output. This month’s increase mainly stems from positive revisions to maize and wheat prospects.

With the bulk of the wheat crop already harvested, world wheat production in 2016 is now put at 749 million tonnes, 2.6 million tonnes above previous expectations and 1.9 percent (14 million tonnes) more than in 2015. This latest revision mostly reflects improved yield prospects for the Islamic Republic of Iran and Kazakhstan. The forecast of world maize production was also raised by 2.9 million tonnes, almost entirely due to a yield-driven upward revision to the United States’ output to a new record level. As a result, global maize production is now forecast at 1 027 million tonnes, 2.1 percent (21.4 million tonnes) higher than in 2015. Expectations of larger plantings were behind a 600 000 tonne boost to the world rice production forecast, now put at an all-time high of 499 million tonnes. In Asia, the revisions mostly concerned Bangladesh, owing to a recovery in local prices, and Nepal, consistent with a favourable unfolding of the monsoon and an adequate supply of inputs. The outlook was also raised for several West African countries, with abundant rains and state assistance supporting strong output gains across the sub-region, most notably in Mali.

Looking further ahead, in the northern hemisphere, planting of the 2017 winter wheat crop in the EU is nearly complete under generally good conditions, with the crop entering dormancy in northern parts. In the United States, although beneficial weather has improved crop conditions compared to the same period last year, low price prospects are expected to lead to a contraction in area planted. In the Russian Federation and Ukraine, the 2017 production outlook is mostly favourable on account of beneficial weather and increased plantings. In India and Pakistan, early projections point to a larger 2017 crop, as improved water availability for the mainly irrigated wheat crop is expected to have instigated an expansion in plantings. The outlook in China is similarly positive, as good weather conditions facilitated fieldwork and benefited the establishment of the early-planted wheat crop.

In the southern hemisphere, the 2017 summer cereal crop is being sown. Maize plantings in Argentina and Brazil are forecast to increase, as prospects of improved returns have encouraged farmers to expand sowings, with favourable weather further boosting the production outlook. In South Africa, favourable weather conditions continue to point to a strong production rebound from the drought-reduced 2016 maize harvest, with 2017 maize plantings forecast to increase by nearly a third over last year’s level. With a few exceptions, sowing operations of 2017 paddy crops have similarly progressed favourably across the southern hemisphere, with expectations of area and yield improvements relative to last year’s El Niño depressed levels.

FAO’s forecast for global cereal utilization in 2016/17 has been raised since the previous report by 2.2 million tonnes to 2 564 million tonnes, up 1.9 percent (47.6 million tonnes) from the 2015/16 level. This month’s upward revision mostly concerns maize and barley utilization and, to a lesser extent, also wheat. Based on the latest assessments, total feed use of cereals is poised to grow by 3 percent (26.8 million tonnes) to 920 million tonnes in 2016/17, sustained by a 3.4 percent expansion in feed use of maize to 588 million tonnes, while that of wheat is anticipated to rise 7 percent year-on-year to 147 million tonnes. Global food consumption of cereals in 2016/17 is forecast at around 1 105 million tonnes, up 1.2 percent from the 2015/16 level and sufficient to maintain average global per caput consumption stable at close to 149 kg, with wheat remaining steady at 67kg and rice at around 54kg.

The FAO forecast of global cereal stocks by the end of seasons in 2017 has been raised by 8 million tonnes to 670 million tonnes, up 1.4 percent (9.2 million tonnes) from the previous season and marking a new record. FAO’s projections of end-season inventories have been raised continuously since the start of the marketing season as production prospects improved progressively, especially for wheat and coarse grains. Under similar circumstances, global wheat inventories in 2016/17 are now placed at a new record of 2 38.5 million tonnes, which is 3.3 million tonnes more than November’s forecast and 5.3 percent (12 million tonnes) higher than at the start of the season. Most of the year-on-year expected annual increase in wheat inventories would be concentrated in China, the United States and the Russian Federation. World coarse grain stocks are projected at 261 million tonnes, some 4 million tonnes higher than previously forecasted and now almost 1 percent (2.4 million tonnes) above their opening levels. All of this month’s upward revision concerned global maize inventories, put at 212 million tonnes, 2.3 percent (5 million tonnes) more than in the previous season. The forecast expansion would be largely underpinned by a 17-million-tonne build-up in maize stocks held in the United States to an all-time high of 61 million tonnes. This would more than offset a likely 13.5-million-tonne drawdown in maize inventories in China to 90 million tonnes. Forecasts of global rice inventories have been similarly scaled up to 171 million tonnes, now pointing to a largely steady level of world rice inventories compared to 2015/16. Based on these adjustments, the world cereal stocks-to-use ratio in 2016/17 would stand at 25.6 percent, confirming an overall comfortable global market situation. This level compares to a low of 20.5 percent registered in 2007/08 and a high of 35.6 percent recorded in 1986/87.

World trade in cereals in 2016/17 is forecast at 388 million tonnes, nearly unchanged from the November forecast but down 2 percent (7.8 million tonnes) from the 2015/16 volume. The contraction mostly stems from expectations that world trade in coarse grains (July/June) would fall 4.7 percent below the 2015/16 all-time high to 177 million tonnes in 2016/17, owing mostly to lower imports of maize, barley and sorghum by China. Expectations are similarly subdued for global trade in rice, which is now seen posting an even smaller (0.6 percent) annual recovery in 2017 to 42.9 million tonnes, on account of lower demand from Far Eastern buyers. By contrast, world wheat trade in 2016/17 (July/June) is envisaged to exceed the previous season’s high level by 0.4 percent (660 000 tonnes), reaching a new peak of 168.5 million tonnes. Ample export supplies and low prices are seen driving brisk trade in wheat this season, with Australia, the Russian Federation and the United States, standing as the main beneficiaries from the exporters’ perspective.

Summary Tables

Source: FAO